What is Medicare?

The answer is complex but you've come to the right spot for Medicare information. We believe that the better educated you are about Medicare, the easier it will be for you to make the right decisions about your Medicare health insurance choices.

Medicare Part A

PART A IS HOSPITAL INSURANCE that assists you with the cost of inpatient care and skilled nursing facility stays. It also helps with hospice and home health care. In general, you should think of the inpatient hospital benefit as Medicare coverage for room and board in the hospital.

It covers the cost of a semi-private room. Part A does not cover many of the actual treatments that might occur, such as scans or surgeries. Those fall under Part B.

The cost of Part A for most people at age 65 is $0. During your working years you have paid taxes to pre-fund the premiums for your hospital benefits. If you don’t automatically qualify for premium-free coverage, most individuals can still apply for it but you’ll pay a sizeable monthly premium to get it.

Medicare Part B

PART B IS YOUR OUTPATIENT MEDICAL COVERAGE. Part B covers essentially all of your other coverage outside of your inpatient hospital fees. You need part B for doctors visits; otherwise, you are uninsured for these. Also, you would lack Medicare coverage for lab work, preventive services, and surgeries.

Part B covers cancer therapy and kidney dialysis. These are extremely expensive medical costs that would be a small fortune without supplemental coverage.

The cost of Part B is set by Social Security and it changes yearly. Individuals in higher income brackets pay more than those in lower incomes brackets. How much you pay is determined by your adjusted gross income reported to the IRS from prior years.

While most people pay the standard Part B premium $164.90 for 2023, other beneficiaries may pay more based on their 2020 Income Related Monthly Adjustment Amount or IRMAA. View the Table for 2023 to determine your Part B premium.

Medicare Part C

PART C IS DEFINED AS A MEDICARE ADVANTAGE PROGRAM, OR PRIVATE INSURANCE. The cost of Advantage plans varies by carrier, county of residence, and plan selected.

To enroll in a Part C plan, you must first be enrolled in both Parts A and B. Even if you find a Part C plan with a very low premium, you will still pay for the Part B premium. You must also live in the plan service area.

Once you enroll, your Medicare coverage will come from the Advantage plan itself, not from the government.

Keep in mind that Part C is voluntary so you don’t enroll at the Social Security office. Many people prefer to get their Medicare coverage from Original Medicare and traditional Medigap plans. These people do not want a Part C Advantage plan, so they will simply not enroll in one.

It is your decision whether you opt for a Medicare Advantage plan as opposed to just staying with your original Medicare A & B and enrolling in Medigap.

Medicare Part D

PART D IS YOUR COVERAGE FOR PRESCRIPTION DRUGS.

It is your pharmacy card.

It covers retail prescription drugs that you obtain from the pharmacy or order via mail order. You choose the carrier and enroll in their drug plan, and that’s how you sign up for a Part D drug plan. Most states have about 30 drug plans to choose from, and the best way to determine which one is the right fit for you is to have your agent run a Part D analysis using Medicare’s prescription drug finder tool.

Long-term Care

Hearing Aids

Routine Dental Care

Routine Vision Care

Medical Care Outside of the U.S.

Denture Care

Plastic and/or Cosmetic Surgery

Massage Therapy

Additional Medicare Information

What is the cost of Medicare for 2023? Premiums, deductibles, coinsurance... How do I calculate all of this?

The premium for Medicare Part B and the premium for Medicare Part D (prescription drugs) along with supplemental coverage is something many don't consider. In fact, many people think all of this is free.

Knowing your options and putting together some estimates is fairly easy and a great way to plan ahead.

Here is a 2023 Medicare (Parts A and B) cost overview:

Part A Premium (Monthly) |

Premium-free with qualifying work history; $506 each month without |

Part A Deductible and Coinsurance |

You pay $1,600 deductible for each benefit period Days 1-60: $0 coinsurance for each benefit period Days 61-90: $400 coinsurance per day of each benefit period Days 91 and beyond: $800 coinsurance per each "lifetime reserve day" after 90 for each benefit period (up to 60 days over your lifetime) Beyond lifetime reserve days: All costs |

Part B Premium (Monthly) |

The standard Part B premium amount is $164.90 (high earners pay more) |

Part B Deductible and Coinsurance |

$226 per year and then 20% of the Medicare-approved amount |

Most people do not have to pay a premium for Part A if they have worked for 10 Years or (40 quarters) in the US. You have already paid for Part A via payroll taxes. To be eligible to purchase Part A, you need to have been a legal resident or have a green card for at least 5 years.

As for Part B, most people will pay a premium of $164.90 per month for 2023. This is based on income and you can locate your Income Related Monthly Adjusted Amount here.

Social Security will deduct your Part B premium from your Social Security check each month.

As for Part D, the monthly premium will vary based on your income. You can determine your Medicare premium costs for Part D with the table located here.

Qualifying for Assistance from Your State

What if you find it difficult to afford the basic cost of Medicare let alone extras like Medigap?

More than 1 in 5 Medicare beneficiaries receives Medicaid. These folks are known as dual eligibles because they qualify for both Medicare and Medicaid. You may qualify for at least one form of assistance from your state, but you have to apply. Here are the options worth exploring:

Medicaid: This is a state run program that supplements your Medicare coverage significantly and provides virtually free health care if you qualify.

Medicaid Medical Spend-Down Programs: If you don't qualify for Medicaid outright, you might be temporarily eligible in some circumstances under the spend-down programs.

Medicare Savings Programs: If you're not eligible for Medicaid, you might qualify to have your premiums paid through one of the Medicare Savings Programs(MSP). A huge advantage to qualifying for an MSP is that you are automatically entitled to Extra Help. Extra Help provides low-cost drug coverage.

A Pace Plan: Programs of All-Inclusive Care for the Elderly(PACE) are especially valuable for those with low incomes and poor health. They are not available everywhere.

State Pharmacy Assistance Programs: These programs help people afford prescription drugs.

Medicaid is administered by each individual state which shares costs with the federal government This means that each state has different eligibility requirements. But in general you will need to show the following to qualify:

- Your monthly income is under a level set by your state.

- Your savings and other resources are under a certain value.

- You live in the state.

- You're a U.S. citizen or legal resident(green card holder).

To find out if you are eligible for Medicaid, call your State Health Insurance Assistance Program(SHIP) which provides personal help from trained professionals. You can also call the Medicaid office at 800-633-4227. Or click here to visit this website which provides information about Medicaid in each state.

Medicare is separate from your application for Social Security income benefits. You age into Medicare at age 65 regardless of whether you are taking retirement income. So, if you are a citizen age 65 or older and are in need of medical insurance you are entitled to enroll in Medicare. You won't receive notification of this so you need to be proactive.

How to apply for Medicare

There are three ways to enroll in Medicare: online, by phone or in person.

Online

The Social Security office offers a quick online application. Just follow one of the links below to apply for

Medicare only:

https://www.ssa.gov/benefits/medicare/

SS and Medicare:

By Phone

Applying for Medicare by phone is also easy. Contact Social Security at 1-800-772-1213 ( for TTY users, it’s 1-800-325-0778) and tell the representative that you wish to apply for Medicare. If the volume of calls is high, Social Security will schedule a telephone appointment with you to take your application over the phone. This process could take longer since the simple forms will need to be mailed to you, completed and then mailed back. Only use this method of application if you are applying a month or two before your intended effective date.

In-Person

There are some people who just like to do things in person. If this is you, then you can go down to your local Social Security office. Doing this can get your application processed quickly. Make sure you receive the print out of your application which shows you have applied for Medicare Parts A and B.

After applying for Medicare, it usually takes about 3 weeks to get your Medicare card. If you are already receiving Social Security on your 65th birthday, you are automatically enrolled in Medicare.

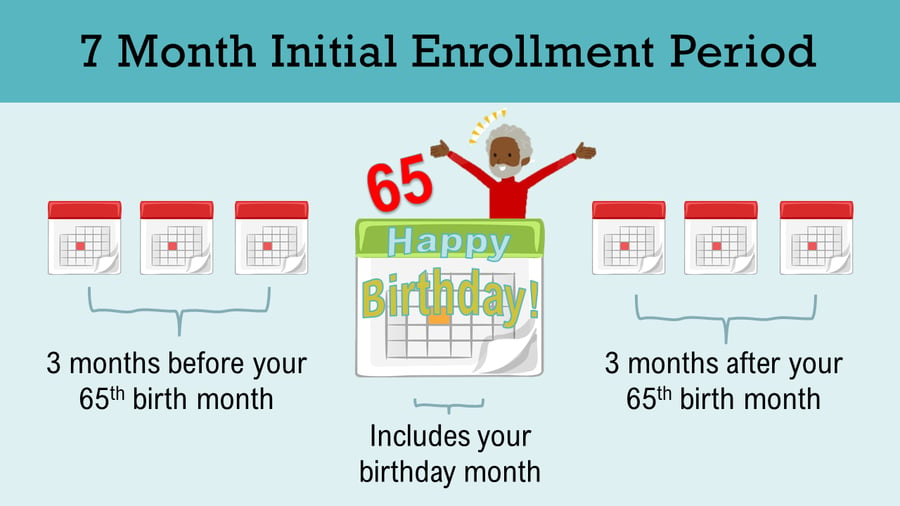

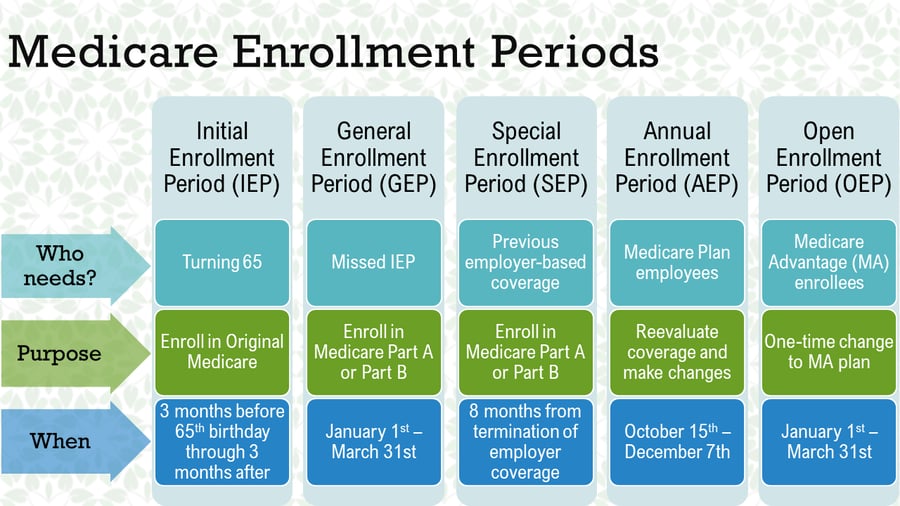

Initial Enrollment Period (IEP)

Your initial enrollment period for Medicare Parts A, B and D lasts for 7 months. It begins 3 months before your birthday month and ends 3 months after your birthday month. Enrolling during this time guarantees you will not pay any late penalties and there are no pre-existing condition waiting periods. This means you have guaranteed issue.

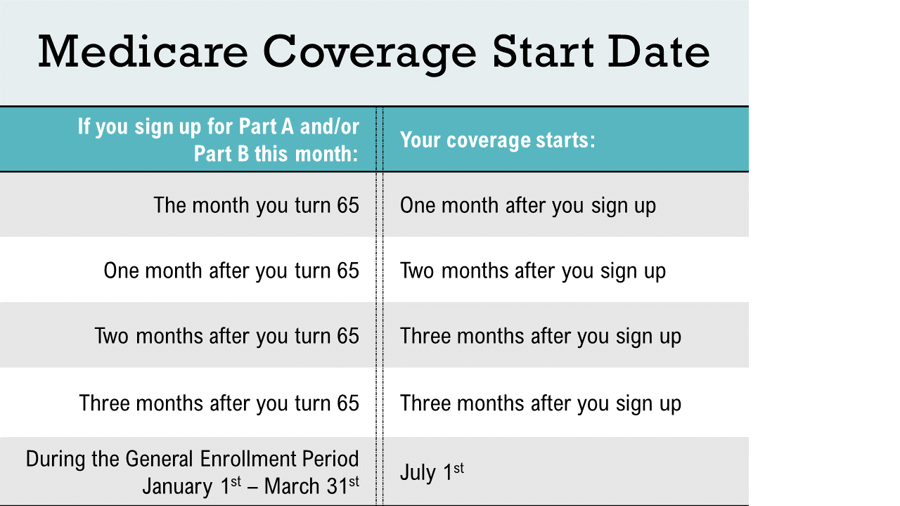

If Medicare will be your primary coverage, you should enroll in Medicare during the first 3 months before your birthday. Your Medicare will then start on the first of the month when you turn 65. This will just ensure you are covered.

If you decide to wait to apply (during those 3 month after your 65th birthday), then your start date will be later which could leave you with a few months of no coverage. Your application date effects your start date.

If you leave an employer during your Medicare Initial Enrollment Period, then your IEP trumps any other election period. In the chart below, you can see when you file for Medicare can affect the effective date of your coverage. It is important to know deadlines.

If you have no other coverage and you fail to enroll during your 7 month IEP, then you will be subjected to a Part B late enrollment penalty of 10% for every 12 month period you were not enrolled.

Beneficiaries working for a small company (20 people or less) should always enroll in both Parts A and B during their IEP since Medicare will be their primary coverage.

If you have Credible Coverage (coverage that is considered as good as Medicare) at age 65 through a larger employer, Medicare will pay secondary. You can then choose whether to enroll in Part B or delay this enrollment until later.

If you don't have Credible Coverage and you delay past 63 days, you will end up paying the late enrollment fee. The penalty for Part D is equal to 1% of the "national base beneficiary premium". Take that number times the number of months you spent without credible coverage and the total is your late penalty cost. Part B penalty is 10% for every 12 months you go without coverage. These penalties do not go away.

Determining your Medicare eligibility is sometimes tricky

There are many questions surrounding when you can collect Medicare, how to qualify for Medicare, what the Medicare requirements are, when to enroll in Medicare, and how to set up Medicare supplement insurance. While the process may seem overwhelming, The Medicare Solutions Group can guide you through this process.

Medicare is our national health insurance system for people aged 65 and older and people with certain disabilities. Medicaid is a joint federal and state program to provide benefits for people with low incomes. It is possible to qualify for both Medicare and Medicaid. When this occurs, Medicare is primary and Medicaid is secondary.

Who is eligible for Medicare:

Part A

You are eligible for Medicare Part A at age 65 if you or your spouse has legally worked for at least 10 years in the U.S.

During those years, you paid payroll taxes toward your Part A hospital benefits. This is why most Americans pay no Part A premiums when they become eligible for Medicare. Part A mainly covers your hospital stays.

Part B

You are eligible for Medicare Part B at age 65 as well. However, you must pay a monthly premium for Part B. This provides for your outpatient benefits such as doctor visits, lab work, surgery fees, and more.

Some people turning 65 still have health insurance through an employer. They can delay their enrollment into Part B and stay in their group health insurance without fearing a late penalty. Understanding the special election period that pertains to this election is key to avoiding a late enrollment penalty.

Although Medicare was originally for only people aged 65 and over, that has changed over the years. The following people can now also qualify:

- Individuals who receive Social Security disability income benefits for 24 months are automatically enrolled in Medicare on the 25th month

- People who receive Social Security disability income benefits and are diagnosed with Lou Gehrig’s disease are enrolled in Medicare on the first month

- People on kidney dialysis or who are a kidney transplant patient are eligible for Medicare. When those benefits will begin depends on your specific circumstances

How many years must you work to be eligible for Medicare benefits:

Your eligibility for Medicare is not based on your work history. However, people with at least 10 years (40 quarters) of paying Medicare payroll taxes will get Part A services without paying premiums once they are eligible.

Do I need to sign up for Medicare when I turn 65?

No, but if you do not have other creditable health coverage, you will face penalties for delaying your Medicare enrollment. You should also know that when you enroll into Social Security income benefits, you will be automatically enrolled into Medicare Part A. You cannot have one without the other.

Initial Enrollment Period (IEP)

The Medicare Initial Enrollment Period is a 7-month window to enroll in Medicare Parts A and B for the first time when you turn 65. You have 3 months before you turn 65, the month of your birthday, and 3 months after to enroll in Medicare. When you enroll in the 3 months after your 65th birth month, coverage is delayed. Enrolling during this time avoids any late enrollment penalties.

This same 7-month window is also used to enroll in a Medicare Advantage or Part D plan.

General Enrollment Period (GEP)

The General Enrollment Period is used to enroll in Medicare Part A and/or Part B if you missed your IEP and do not qualify for a special enrollment period.

The GEP window starts January 1st and ends March 31st of each year and coverage is delayed until July 1st.

Special Enrollment Period (SEP)

A Special Enrollment Period is used anytime a beneficiary has a qualifying event. If you delayed Medicare past age 65 due to creditable coverage through active employment, you could use this enrollment period to apply for Medicare A and B.

There are also Special Election Periods (SEP) for Medicare Advantage and Part D plans. If you have a qualifying event, you will have a 2-month window to enroll in either a Medicare Advantage plan or Part D plan.

Annual Enrollment Period (AEP)

The Annual Election Period begins October 15th and ends December 7th of each year.

Medicare beneficiaries that already have Part A and Part B can use this election period to enroll in, change,or disenroll from a Part D or Medicare Advantage plan.

Open Enrollment Period (OEP)

This enrollment period is for beneficiaries who already have a Medicare Advantage plan but want to leave it.

During the MA OEP window, from January 1st-March 31st, you can switch from your current Advantage plan to another or enroll in Original Medicare with a Part D plan